The CFO's AI Implementation Guide: Architecture That Actually Works

Most finance AI deployments fail — not because the technology doesn't work, but because CFOs automate old processes instead of redesigning around them. Here's the architecture that actually delivers measurable value for mid-market finance teams.

You've probably seen this play out. A major ERP migration, a new AI module switched on, a vendor demo that looked genuinely impressive. And then, six months later, one of your peers admits in a closed-room conversation: "We've taken our old processes from the old ERP and put them in a new system."

The technology changed, the workflow didn't, and nothing measurably improved.

This is the dominant pattern in finance AI right now. Deloitte's 2026 Finance Trends research found that 63% of finance departments have deployed AI solutions — but only 21% believe those investments delivered clear, measurable value. And the L.E.K. Consulting 2025 CFO Survey found something even starker: among CFOs who have piloted AI, only 4% report a pilot success rate above 50%.

Four percent.

The problem isn't the technology. The problem is what CFOs are doing with it.

Why Most Finance AI Fails Before It Starts

The failure mode is simple. A finance team identifies a painful process, drops an AI tool on top of it, and expects the output to improve. Sometimes it does, a little. Usually it doesn't, enough.

The reason is simple. You don't get value by automating an old process. You get value by redesigning the process around what an agent can actually do.

An agent can monitor continuously. It can cross-reference data across systems. It can flag anomalies the moment they appear, not at month-end when someone finally runs the report. It can draft the variance explanation and prepare the board pack without being asked, and it can surface the invoice that's 47 days overdue before anyone goes looking for it.

But if you take that capability and slot it into a workflow that was designed for a human doing one task at a time, you've just made the old process slightly faster. You haven't changed what the finance team can see, decide, or do.

One CFO in the L.E.K. survey put it bluntly about vendor claims: "A lot of what we see from vendors, when you talk about their AI offerings, it's RPA 2.0."

That's the right skepticism to carry into every vendor conversation.

The Architecture Decision That Actually Matters

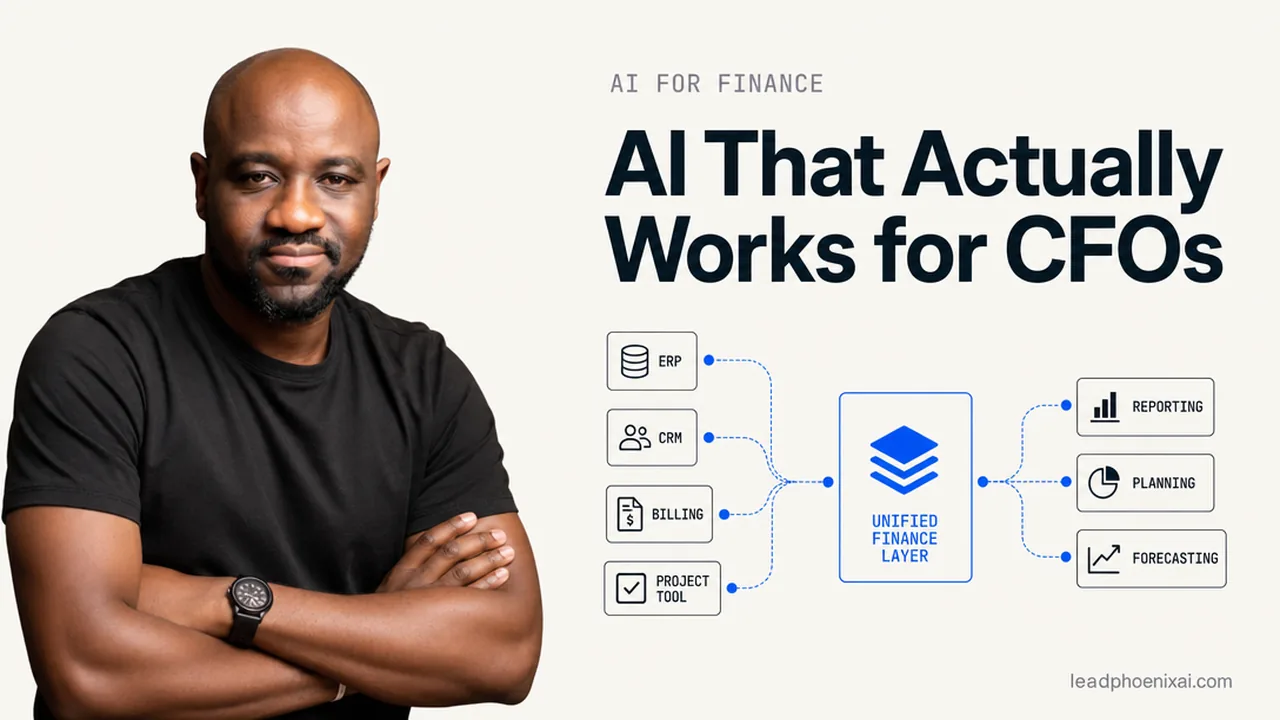

Before you pick a tool, you need to make one foundational decision: where does your data live, and can anything actually read across all of it?

Most mid-market finance teams have their data spread across completely separate systems. The ERP holds the GL. The CRM holds the pipeline. The project management tool holds delivery timelines and team capacity. The billing system holds invoice history. None of these talk to each other in any meaningful way.

A question like "which clients are most at risk of churn based on project delays and open AR aging?" can't be answered — not because no one thought to ask it, but because the data to answer it lives in three systems that have never been connected.

This is why the source-of-truth layer comes before any automation. Connect the systems first. Get all of that data into one place that every workflow, every agent, and every report pulls from. Once that exists, the finance function becomes dramatically more intelligent — not because you added a smarter tool, but because you can now cross-reference across disciplines that were previously invisible to each other.

Without it, every AI workflow you build is only as smart as the one silo it can see.

Buy the Spine. Build the Edges Selectively.

Once the data layer is sorted, the architecture question becomes: what do you buy, what do you build, and what do you borrow?

McKinsey's research on AI and ERP architecture offers the clearest framework I've seen: Buy standardized capabilities like embedded approval agents, predefined data products, and ERP-integrated orchestration, and reserve custom development for the select areas where domain-specific logic or proprietary workflows create real competitive advantage.

For most mid-market finance teams, that means:

Buy the spine. Your ERP backbone — whether that's NetSuite, Sage Intacct, or QuickBooks Online — stays the system of record. The AI capabilities embedded in those platforms handle the standard workflows: AP automation, bank reconciliation, basic anomaly detection, approval routing. These are solved problems. Don't rebuild them.

Build or borrow the edges. Where your business has genuinely unique logic, such as a proprietary revenue recognition model, a complex multi-entity consolidation structure, or a specific forecasting methodology that reflects how your industry actually works, that's where custom agent work is justified. Not everywhere. Not as the default.

The Zuora survey found that 53% of finance leaders trust AI embedded in existing systems most, versus 13% who trust AI-native solutions. That's a reasonable starting position for most mid-market CFOs. But it's worth knowing that the 13% who favor AI-native platforms tend to be growth-stage practitioners who've found that newer platforms like Campfire handle revenue recognition, consolidations, and multi-currency more intuitively and at lower cost than legacy ERP. The right answer depends on where you are in your growth trajectory and how much technical debt your current stack is carrying.

Where the Real Wins Are Right Now

Let me be specific about what's actually working, because the evidence is concrete.

Accounts payable and receivable. AI adoption in AP increased fourfold between 2024 and 2025, according to the Institute of Financial and Operations Leadership — from 7% to 29% of teams surveyed. One CFO at a global produce distributor described the outcome directly: "A task that used to take three hours now takes 15 minutes. The team is no longer stuck processing invoices the whole day."

That's not a transformation story. That's a specific process, a specific time saving, and a team that now has capacity for something more valuable.

Month-end close and variance analysis. AI that flags anomalies and pinpoints variances in real time — rather than waiting for someone to run the month-end report — cuts the close timeline and frees the team for analytical work instead of reconciliation. The CFO of an energy software company described exactly this: faster anomaly detection, shorter close, more time on analysis.

FP&A and forecasting. This is where the data architecture decision pays off most visibly. Traci Gusher, EY's Americas AI and Data Leader, made the point clearly: internal data is valuable, but external data is what makes a forecast meaningfully more accurate. If your forecasting agent can only see your internal GL, it's working with one hand tied behind its back. Connect external signals — market data, industry benchmarks, macroeconomic indicators — and the forecast becomes genuinely more useful.

Board reporting and leadership dashboards. This is the "wow moment" for most finance leaders. When the agent can pull from the ERP, the CRM, the project management tool, and the billing system simultaneously, you can answer questions that were previously impossible. "Show me every client where revenue grew but our hours dropped — that's where we're under-billing." "Show me every project where the same cost category spiked in three consecutive months." These aren't hard questions. They just required data that was previously siloed.

The Governance Layer Is Not Optional

A lot of mid-market AI implementations cut corners on governance, and that's where the real risk lives.

If you're deploying AI agents in a finance function, the control layer has to be built in from the start — not added later when someone asks about it.

Four things are non-negotiable:

AI drafts, humans approve. The agent prepares the journal entry, flags the anomaly, drafts the variance explanation. A human reviews and approves before anything posts to the books. This isn't a limitation of the technology — it's the right operating design. The deliverable is not "AI runs your finance function." It's "AI handles the 85% so your team can spend their time on the 15% that requires judgment."

Source citations on every number. Every output links back to the source row, file, or system. If the agent can't show its work, the CFO won't trust it — and shouldn't. This is the single biggest trust unlock in any finance AI deployment.

Audit trail. Who ran it, when, with what inputs, what was approved, what was overridden. Standard logging. Not glamorous, but every regulated finance team will ask for it, and you want to have it before they ask.

Read from source, don't replace it. The GL stays the system of record. The agent reads, normalizes, and drafts. It doesn't write back to the system of record without explicit sign-off. The moment an agent starts posting directly to your books without a human in the loop, you've created a books-and-records risk that your auditors will find.

Custom AI tools that skip this layer are also where the shadow IT problem starts. A well-meaning analyst builds a Python script that pulls from three systems and generates a weekly report. The analyst leaves. Nobody else knows how it works. The report keeps running. Nobody knows if it's still accurate. That's not an AI strategy — that's a liability.

The Sprint Model: How to Actually Implement This

The mistake most firms make is trying to transform everything at once. A company-wide AI roadmap, a transformation program, a change management initiative. It sounds serious. It rarely ships.

The approach that works is simpler. Pick the outcome you want to move. Identify the low-dollar-per-hour work that's blocking it. Automate that specific bottleneck in a focused sprint. Measure the lift. Improve. Sprint again.

For a mid-market finance team, that might look like:

- Sprint 1: Connect the ERP and billing system to a shared data layer. Run a query you've never been able to run before. Show the team what's now visible.

- Sprint 2: Deploy an AP automation agent. Measure the time saved per invoice cycle. Get the team comfortable with the suggest-and-approve loop.

- Sprint 3: Build the month-end anomaly detection workflow. Cut the close by two days. Document the before and after.

By sprint 3, you have three concrete wins, a team that's adopted the tools because they were built around processes the team actually finds painful, and a data layer that makes every subsequent sprint faster.

This is not a transformation program. It's a compounding loop. And the compounding is where the real value lives.

Frequently Asked Questions

What's the biggest mistake CFOs make when implementing AI in finance? Automating an existing process without redesigning it. When you drop an AI tool into an unchanged workflow, you get the old process running slightly faster — not a meaningfully different outcome. The CFOs who are seeing real results started by asking what the workflow should become now that an agent can monitor, flag, and draft continuously, then decided where the human belongs in that new design.

Should a mid-market CFO buy an AI-native finance platform or stick with embedded AI in their existing ERP? For most mid-market firms, the right starting point is the AI capabilities embedded in your existing ERP — NetSuite, Sage Intacct, QuickBooks Online. These handle the standard workflows and keep your system of record intact. AI-native platforms like Campfire are worth evaluating if your current ERP is carrying significant technical debt or if you're dealing with complex multi-entity or multi-currency structures that legacy ERPs handle poorly. The architecture principle that holds in either case: buy the standardized spine, build custom agents only where you have genuinely proprietary workflows.

How do you prevent AI agents from creating audit and compliance risk in a finance function? Four things: agents draft, humans approve before anything posts to the books; every output cites its source row or file; every run is logged with inputs, approvals, and overrides; and the GL stays the system of record — agents read from it, they don't write back without explicit sign-off. Build the control layer in from the start. Adding it later is significantly harder and more expensive.

What finance workflows should a mid-market CFO prioritize for AI first? Start where the manual work is most concentrated and the data is cleanest. For most mid-market teams, that's AP and AR automation, bank reconciliation, and month-end anomaly detection. These are solved problems with proven ROI — one CFO cut a three-hour AP task to 15 minutes. Once those are running and the team trusts the suggest-and-approve loop, move to FP&A variance analysis and board reporting, where the cross-system data layer starts delivering insights that weren't previously possible.

How do you avoid the shadow IT problem when finance teams start building their own AI tools? Scope discipline is the answer. Every agent deployment should have a defined owner, documented inputs and outputs, an audit trail, and a clear handoff plan if the person who built it leaves. The risk isn't that finance teams experiment — it's that experiments become production workflows without governance. Set the expectation early: if it's running in production, it needs documentation, logging, and a named owner. Anything that can't meet that bar shouldn't be running unsupervised.

Sources

Cited inline above:

- Deloitte — 2026 Finance Trends

- L.E.K. Consulting — 2025 CFO Survey

- McKinsey — AI and ERP Architecture

- Institute of Financial and Operations Leadership — AI in AP Research 2025

- Zuora — Trustworthy AI Survey

Additional sources consulted for this piece:

- EY — AI and Forecasting (Traci Gusher, EY Americas AI and Data Leader)

- Bain — Technology Maturity Assessment 2025

- CPA Practice Advisor — Generative AI Adoption, May 2026

- Battery Ventures — CFO Survey (129 CFOs)

- F Suite Community — CFO practitioner forum