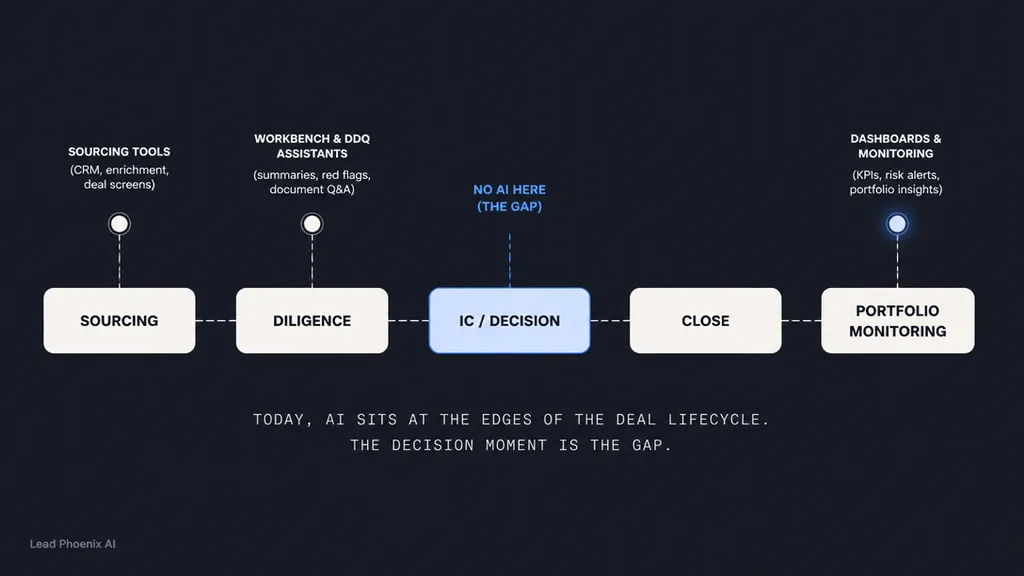

The Deal Room Is the Last Place PE Has Put AI

S&P Global says only 31% of PE firms have AI integrated into due diligence — and that is the highest-adoption category across the deal lifecycle. FTI Consulting says 95% of funds report AI initiatives meeting or exceeding the original business case. Both numbers are about the same firms. They are saying AI is working at the edges of a PE business — IR automation, DDQ drafts, portfolio dashboards — and not yet where the buy/no-buy call gets made.

April's S&P Global 2026 Private Equity Survey shows due diligence as the highest-adoption AI function across the entire PE deal lifecycle — at 31% "somewhat or fully integrated." That is the highest category. Deal sourcing was rated ineffective by 64% of respondents. Portfolio monitoring by 75%.

A month earlier, FTI Consulting's 2026 PE AI Radar surveyed 200 fund and operating leaders and reported 95% of funds saying their AI initiatives are meeting or exceeding the original business case.

Both numbers are true. They are not saying contradictory things.

They are saying AI is working at the edges of a PE firm — IR automation, DDQ drafting, portfolio dashboards, deck assembly — and not in the deal room itself. The function that decides whether a check gets cut is the function with the smallest AI footprint.

What 31% actually means

Read "somewhat or fully integrated" carefully. That category folds in firms running a Gemini summary on the VDR, firms using ChatGPT to draft management questions, and firms running a workbench against the CIM. Some of that is just keyword extraction over a 400-page data room. Almost none of it is AI inside the diligence call.

A good diligence call is a two-hour conversation among the deal team, the operating partner, and (sometimes) a sector consultant. People in the room are trading judgment on management quality, customer concentration, working capital quirks, and KPI trajectory. The output is a buy / no-buy with conditions.

The S&P number tells you that roughly three in ten PE firms have AI somewhere upstream of that conversation. It does not tell you that AI is in the conversation. We have not seen a PE firm yet where an analyst agent is in the room making the call alongside the team.

The gap is not technical

The technical layer is more or less ready. A voice analyst with sector context can sit on a financial dashboard, answer spoken questions in real time, navigate between an overview, an advisory tab, and a ridgeline chart, and produce a defensible cautious-buy with named caveats. We built a working version of this earlier in the month — Nova, a voice analyst — recorded against a fictional $40M CPA acquisition target. Four moments, escalating: summarise, diagnose, notice, judge.

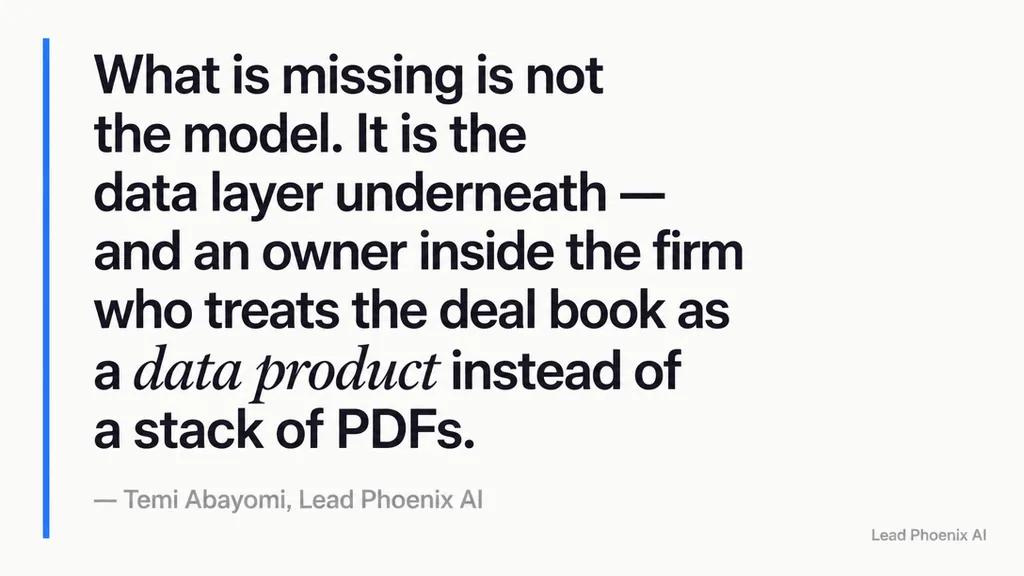

What is missing is not the model. It is the data layer underneath the model, and an owner inside the firm who treats the deal book as a data product instead of a stack of PDFs.

The diligence team gets the CIM, the data room, the management presentation, the QofE, and a half-dozen partner-prepared schedules. None of those documents are connected. A junior associate spends the first two weeks of every deal flattening them into a working model. By the time the deal team is in the room with the seller, the data layer is bespoke for this deal and useless for the next one.

That is the bottleneck. The model is downstream.

What "AI in the deal room" actually requires

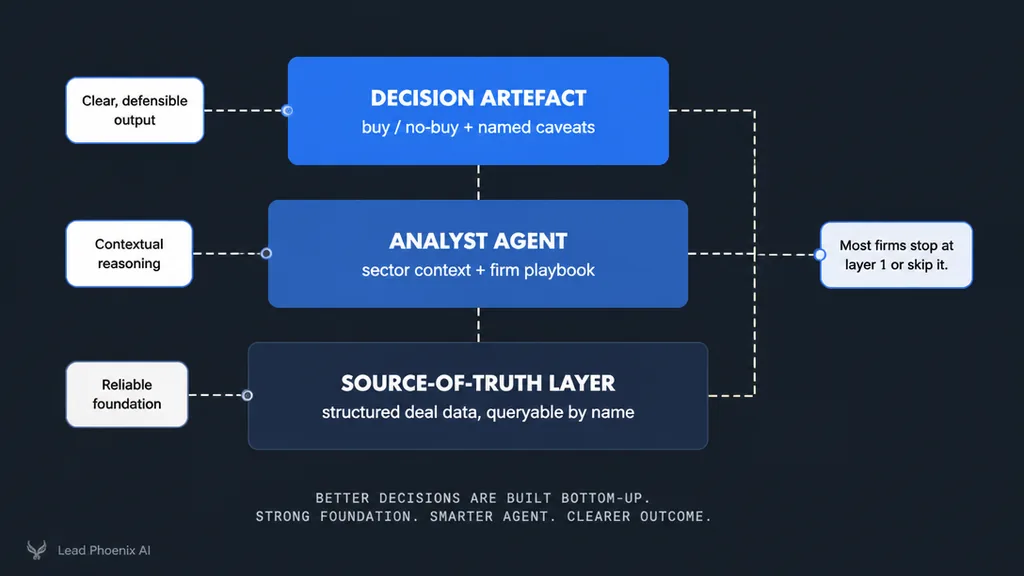

Three things, in order:

- A source-of-truth layer for the deal. Financials, KPIs, customer concentration, headcount, utilisation, working capital — pulled into a structured form once, queryable by name, versioned as new information arrives. This is unglamorous infrastructure. It is also the only thing that makes the next two layers possible.

- An analyst agent with sector context. Pre-loaded with the firm's diligence framework, the relevant sector playbook, and the comparable deals already in the firm's history. Configured to navigate the deal book and reason over it — not to summarise it. This is the same pattern as the broader shift to AI agents in finance — the agent is configured, not just summoned.

- A decision artefact, not a memo. Output should be what a deal partner actually uses: a buy / no-buy stance with named caveats, the dashboard view the partner saw when forming the call, and the data points the call rests on. Not a 12-page memo nobody reads.

Most PE AI today stops at the first layer or skips it entirely. Firms buy a deal-sourcing tool, install a portfolio monitoring dashboard, paper over the gap with a junior associate. The model gets used as a fancy search bar. Most PE AI today is stuck somewhere between a pilot and production — useful, but never quite in the room where the call gets made. The 31% number is consistent with that.

What operating partners actually want

We have asked. The answer is consistent. They do not want AI to write the memo. They want AI in the diligence call, watching the dashboard while the seller's CFO is talking, flagging the thing the prep deck missed.

That is a categorically different deployment from "AI for DDQ automation" or "AI for portfolio reporting." It requires the data layer to exist before the call starts, an interface the partner can talk to in real time, and a model that is allowed to disagree.

It is also where the operating leverage actually sits. A diligence cycle costs a mid-market PE firm somewhere between $200K and $800K in deal-team time, third-party fees, and management distraction. Removing two weeks of junior model-building from that cycle is real money. Catching a customer concentration issue before the LOI rather than after the QofE is more.

What firms should do next quarter

If you run a mid-market PE firm doing 4–8 deals a year, the move is not to buy another deal-sourcing platform. Pick one deal currently in diligence and build the source-of-truth layer for it. Not in PowerPoint. In a queryable form. With the named KPIs, the named risks, and the named comparables wired up.

Then run an analyst agent against it for one diligence call. Track what it caught that the prep deck missed. Track what it caught that the deal team had not thought to ask. Track what it got wrong.

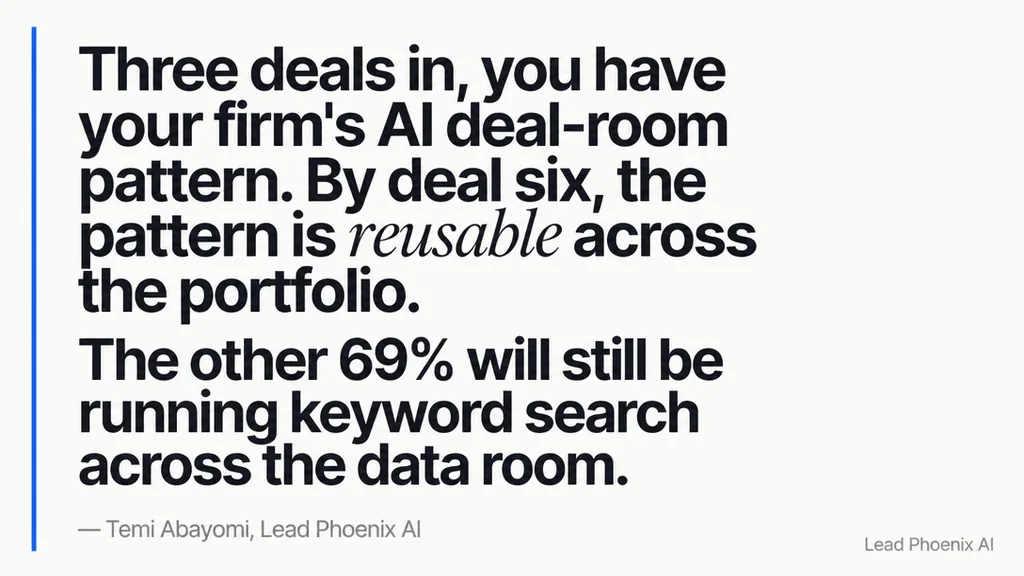

Three deals in, you have your firm's AI deal-room pattern. By deal six, the pattern is reusable across the portfolio. By the end of the year, the function S&P called "due diligence" is actually integrated — not just somewhere upstream of the call.

The other 69% will still be running keyword search across the data room.

This is the conversation we have with operating partners and PE-portfolio CFOs once a week. If the deal-room layer is what is missing in your firm, the AI Readiness Audit identifies which deal-lifecycle function actually has the most operating leverage — and what the source-of-truth layer would look like for your sector.

Frequently Asked Questions

What does the 31% "AI in due diligence" number actually include?

S&P Global's 2026 PE Survey counts any firm running an LLM somewhere upstream of the call — VDR summaries, ChatGPT-drafted management questions, document workbenches against the CIM. It does not mean AI is in the diligence call itself. Almost no PE firms have an analyst agent in the room when the buy/no-buy call gets made.

How is "AI in the deal room" different from AI for DDQ automation or portfolio monitoring?

DDQ automation and portfolio dashboards run at the edges of the deal lifecycle. AI in the deal room means an analyst agent reasoning over a structured deal dataset in real time during the diligence call — answering spoken questions, navigating between dashboards, and producing a decision artefact with named caveats. It is a categorically different deployment from a report-generator.

What does the source-of-truth layer for a deal actually look like?

Financials, KPIs, customer concentration, headcount, utilisation, and working capital pulled into a structured form once, queryable by name, versioned as new information arrives. Not a PowerPoint summary of the CIM. Not a flat spreadsheet. A queryable dataset that an analyst agent can reason over and a partner can ask questions of in plain English.

How long does a first deal-room AI pilot take at a mid-market PE firm?

Pick one deal currently in diligence. The source-of-truth layer for that deal can be wired up inside two weeks with a focused team. Running an analyst agent against it for one diligence call adds another week. By the third deal, the pattern is repeatable; by deal six, it is reusable across the portfolio.

We already have Hebbia / V7 / Harvey. Is this different?

Those tools are excellent at document search and extraction — the first half of the upstream work. They do not, on their own, give you an analyst agent that reasons over a structured deal dataset during the diligence call. The data layer underneath is still your firm's responsibility to design, and the agent configuration is still the operator's job.

Where does this start in practice?

An AI Readiness Audit scoped to your portfolio operating model — sector-specific data layer, governance design, and the two or three KPIs where AI actually moves EBITDA next quarter. Two weeks, $7,500, packaged into a 90-day implementation roadmap.